The world has steadily observed the Argentinian situation the last months, effectively turning the country into an experimental lab of public policy. In past articles Milei’s proposals were discussed, explaining their main ideas and highlighting the reason why these, despite being unconventional, could present a solution to Argentina’s problems. This article aims at evaluating the Argentinian situation five months into Milei’s mandate, as well as to deepen into the monetary and fiscal spheres underlying the Argentinian struggle. It is convenient to recall that while both the fiscal and monetary sphere are separate policy instruments to govern a nation, there is a close relation between these, as fiscal soundness is a prerequisite for monetary stability. This statement is the foundation of Milei’s envisioned solution and thus necessary for understanding this article. First, the general monetary situation will be dealt with, then the analysis will delve into the details of the fiscal situation and the steps so far taken for deregulation of the economy.

As outlined in the past, the main objective for Milei’s team is to lower the immense pressure on prices which made up for a monthly inflation rate of 25% and a poverty rate of 50% as of December 2023. For these purposes, a goal set on the horizon is also to abolish the central bank and establish the dollar as the national currency.

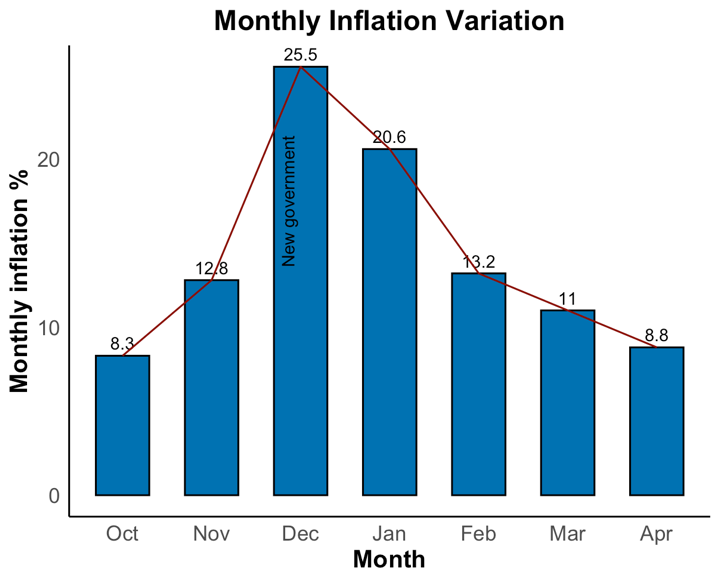

Figure 1. Monthly variations in inflation rate. Built with INDEC data retrieved on 28/05/24.

The figure above depicts the course of the variation of inflation in Argentina. There is an evident deceleration in the inflation rate. But what about the spike at the beginning of the mandate? How did the downward trend later materialise?

The first hike

Contrary to his own ideology, Milei actually resorted to monetary emission right after his positioning. To explain how and why this happened we first diverge to the CB situation. The CB in Argentina cannot be abolished from one day to the other for two major reasons. First, it is the main buyer of government debt, if the demand does not satisfy the supply of treasury bonds the country would face default. Second, it has outstanding liabilities which reached over 30 billion USD in December 2023.

In an attempt to move forward in extinguishing the CB’s liabilities, the government has called a stop on the emission of the LELIQS, these were liabilities with maturity of 28 days which the CB issued to commercial banks at 133% rate, and consequently used to buy treasury bonds from the government. This surged as a mechanism to avoid monetisation of debt. That is, instead of printing money to buy treasury bonds, borrow to commercial banks and pay an interest rate later in return. However, the problem with these was that eventually the principal and the interest would often have to be repaid through monetary expansion nonetheless, since the central bank would not have any other significant inflows. How did the government manage to extinguish these liabilities? First halt further emission. Second, pay back outstanding LELIQS. This was done, ironically, by printing more money, which is certainly a factor underlying the inflation rate hike exhibited that month in Argentina.

Another measure which contributed to the hike was the elimination of the “cepo cambiario” i.e., strong devaluation of the peso which went from 386 ARS/USD to 800 ARS/USD to move the official exchange rate closer to market realities. It was natural to expect this measure to backfire with inflation rate hikes, however, the government carried this seeking to restore confidence in the markets by eliminating artificial barriers on transactions and encouraging foreign investment.

Why did the administration indulge in monetary emission if now more than ever Argentina knows that printing money is the recipe for disaster?

It could be argued that the money printed and paid to commercial banks would not enter immediate circulation and thus not affect prices too drastically. The reason for this is that commercial banks used these as reserves to back up deposits. Moreover, since deposits yield an interest rate, banks would have to reinvest these funds to avoid incurring losses. For this reason, another CB instrument came into play, the so-called “pases”. These pases had maturities of one to seven days, and only paid an interest of 100%, lowering the burden on the CB’s balance sheets. Essentially, not all printed money entered circulation since a considerable part was reinvested in financial instruments. Note however, that commercial banks could not keep sound balance sheets just with the pases given the relatively low return rates, they needed to seek new investment opportunities, we will see later how the government took advantage of this excess demand for financial assets.

How has the downward trend materialised?

As of December 2023, fixed-term deposits ensured citizens a return of around 110%, this was clearly still not convenient for a country with a high inflation rate, since it was a clear loss in real terms. For this reason, the second big announcement of monetary policy was the emission by the government of new treasury bonds or “letras del tesoro” which could be directly acquired by commercial banks and specially, the citizens. The instruments involved short-term (28 days) securities with a spot rate of 180%, and medium/long-term securities ranging from one to three years indexed to the inflation rate. The issuance of such instruments conveyed several advantages in the fight against price pressure. First, by leaving out the central bank as financial intermediary (which was in practice its role in the LELIQS case), the central bank would not expand its liabilities and thus avoid completely the necessity of resorting to monetary expansion. Secondly, the longer-term, inflation-indexed securities provide a valid incentive for the population not to spend and invest, taking away money from circulation and decelerating inflation. It must be underscored however that there is a great responsibility in issuing bonds at higher rates, there must be a strict commitment of the government to heal its fiscal balances and prove its capacity to pay back this debt, as will be discussed later in this article.

A parallel factor to this discourse is given by the depreciation of the peso in foreign exchange markets. Before, another major reason why the CB wouldn’t lower the famous 133% rate was because, amidst expectations of continued inflation, there was a fear the public would indulge in massive purchases of more stable currencies as the USD, which would exacerbate the devaluation on the domestic currency and in turn produce inflation by increased import costs and higher debt servicing costs (remembering Argentina’s main debt is denominated in USD). The great achievement by Milei’s administration is that it has managed to lower interest rates without causing almost any depreciation of the peso.

Today, by progressively taking pressure away from the CB, short-term interest rates on CB liabilities have been the lowest at around 50%. Despite this, depreciation has not materialised since confidence in domestic markets and the peso has been at least partially restored. Moreover, the effectiveness of monetary policies have also lowered inflation expectations. Essentially, a lower expected money supply, given by Milei’s commitment to avoid monetary emission, and a higher expected money demand given by the lowering rates, signifies a greater expected value of the peso. But as mentioned before, this mechanism has not acted unilaterally, it is impossible that the devaluation and the lowering rates would bring any higher confidence if the government did not support its measures with a credible commitment, and this was given by the strict fiscal austerity which today is about to hit 4 consecutive months of fiscal surplus.

The fiscal sphere and the DNU

The decree, which declares a state of emergency on many state matters until December 31 of 2025, is based on strong deregulation aimed at creating an economic system based on free competition, respect for private property, and free movement of goods, services, and labour. One of the objectives, besides obviously restoring the country’s finances, is to comply with the recommendations of the WTO and OECD.

As mentioned in a previous article, Milei’s idea is to significantly reduce the role of the state in the economy. Article 5 of the decree provides for the derogation of Law No. 26,992, which had introduced the Price and Availability Observatory for Goods and Services. The purpose of this institution, as one can easily imagine, is to monitor prices and availability of goods and services available to prevent behaviours that may create distortions within the market. Among the powers of the observatory, there is the ability to request from companies all documentation related to their commercial activities.

Law No. 27,545, which establishes transparent, competitive prices for food and beverages products, personal hygiene and household items for the benefit of consumers, is repealed. Its objective was to prevent companies from engaging in harmful business practices that disadvantage consumers or pose risks to competition and distortions within the market.

This law is known as the “gondolas law.” “Las gondolas” refers to the supermarket spaces designated for product displays. Point A of article 7 impose that “the display of products from a supplier or group of companies cannot exceed thirty percent of the available space shared with similar products. Participation must involve no fewer than five suppliers or groups of companies.” The goal is to prevent a single supplier from occupying all the display space in a section of the supermarket and setting excessively high prices for consumers.

Point C, on the other hand, stipulates that products with the lowest prices should be positioned on a shelf equidistant between the first and last, making them more visible to consumers. It is evident that the regulator aims to favour consumers by implicitly encouraging them to purchase more affordable products.

Regarding the state reform, Milei has envisaged a derogation to Law No. 23,696 concerning state-owned enterprises. According to the law, state-owned enterprises act under the direct control of the State and the Contaduría General de la Nación, which operates from an accounting standpoint.

The derogation to this law lays the groundwork for the privatisation program of enterprises, strongly desired by the new government, which has significantly reduced following the rejection of the Omnibus law. The list of enterprises attached to the Omnibus law that Milei wants to privatise includes the aeronautical company, postal services and state railways. The objective is to decrease public spending, especially for loss-making enterprises, and bring immediate liquidity to the state’s coffers.

Analysing the part of the DNU dedicated to labour laws, there are significant changes to Law No. 20,744. For instance, Article 92 BIS has been modified to extend the probationary period for indefinite contracts from 3 to 8 months, thereby increasing job insecurity. However, all necessary protections to prevent abuse of the probationary period are still maintained.

Another modification to the law is anticipated in Article 124. This previously stipulated that the account into which the worker’s salary was deposited should be free of opening, management, or fund withdrawal fees. Furthermore, it was envisaged that, in some cases, the state could decide the payment methods for remuneration among the aforementioned cases, also applying supervisions, under penalty of nullity of the transaction.

Milei’s reform has only retained the indications regarding the payment methods of the salary (thus, the fact that it can be received in cash or through a financial institution) but has eliminated the part of the article referring to management costs and the state’s ability to “force” the employer into one of the methods in certain situations.

Despite the Omnibus law not being passed in its original form, the policies implemented so far have yielded some positive results. The state budget has achieved surpluses after 15 years of deficits, and market confidence seems to have improved. Additionally, inflation has experienced a slight decrease. Furthermore, Argentina and the International Monetary Fund have reached an agreement on the debt review of 44 billion dollars, which will result in a new disbursement of 800 million dollars after approval by the Executive Board.

However, it must be noted that the implemented measures are highly restrictive and unpopular. It will be interesting to see if the citizens’ trust in the government matches that of the international markets.

Curated by Jerry Vera Bacigalupo and Riccardo Puletti.

Recent Comments